Things are going crazy in my world. We closed on our 50th self-storage facility this week with the acquisition of a 3 property portfolio in Virginia. That makes 1,329,609 square feet and 9,905 units managed by our team of 40 employees.

All operated remotely with our team of 40 employees – 18 in the Philippines, 6 in Colombia, and 16 in the states (from Utah to Boston to Miami). All of the Filipinos were recruited through Shepherd, which I highly recommend checking out if you need admin, customer service, or back-office staff.

Our pipeline is empty. We’re working harder than ever to find deals but keep striking out. We’re underwriting 25+ deals per week and sending 10 offers per week. We do have some big, promising deals in the pipeline that we’re excited about, though.

Enough about that… lets break down a recent deal that went full cycle last week with a cash-out refi that put $2.6 million in our bank account, tax-free.

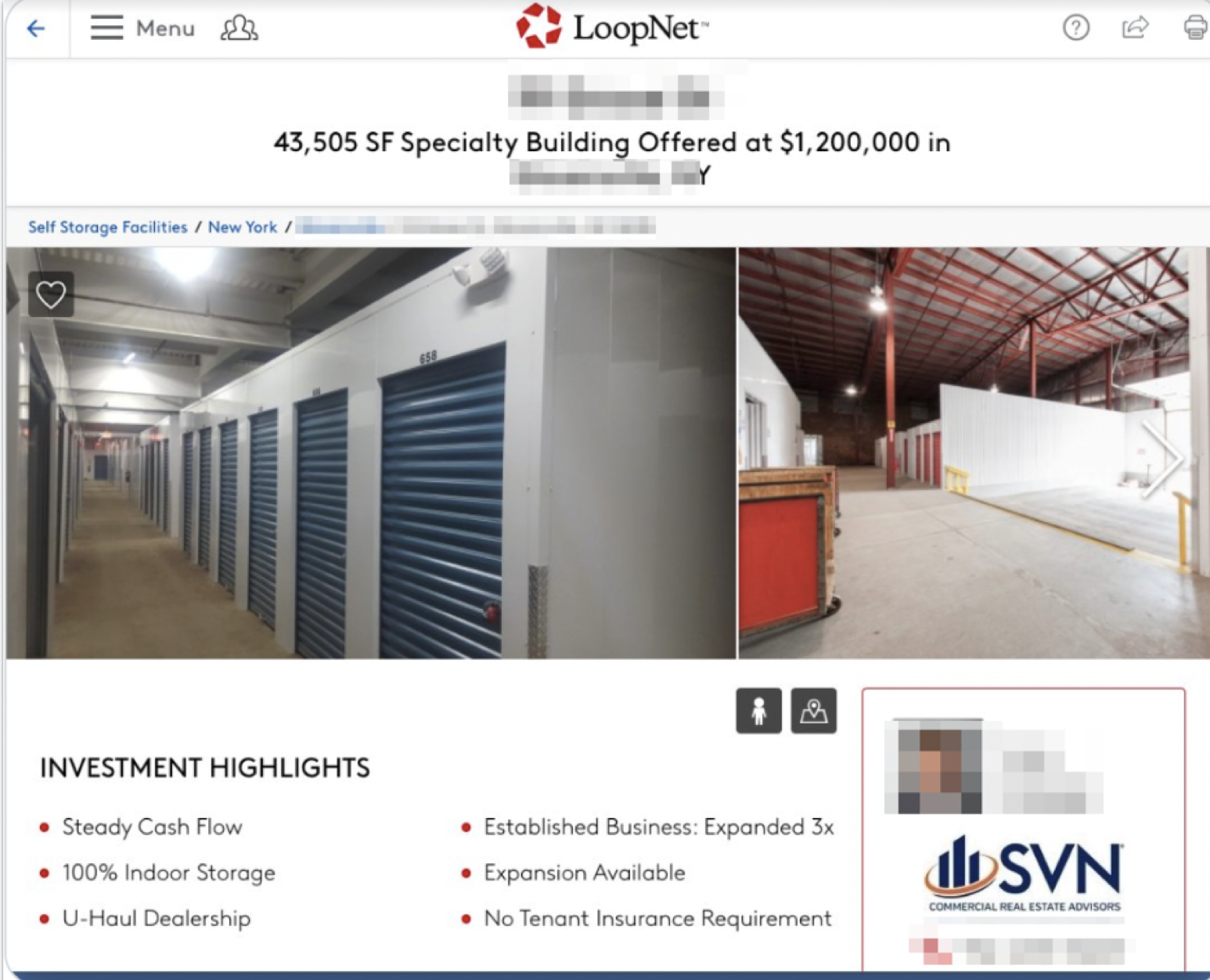

On Sep 3rd, 2020 we closed on a 120k sf glove factory built in 1890 in a small town in upstate NY.

I first saw the property listed for sale on Loopnet in mid-2018. I ignored it. Who wants to try to operate a building in an old factory in a dying NY town? A few months later I looked at it again and decided to reach out. The broker sent me the financials. They were good. $25k a month in revenue and $10k in expenses.

Here is a screenshot of the listing:

The deal had some hair on it.

It was cash flowing really well but it needed a new roof and there were surely environmental concerns at the old factory. I toured it and took this video. It was old. It was huge. It was incredibly intimidating.

Full-time manager. No online rentals. Very limited access hours (8a-5p M-F).

The roof replacement was quoted at $250k. We knew a phase 1 inspection was needed and would likely require a Phase 2 (which means actual environmental work). Even though it was listed at $1.2m and cash flowing at $15k a month it still wasn’t worth it to us. We let some time pass (3 or 4 months).

Then the broker called me back.

He was persistent and said we should make an offer even if it was low. So we submitted an LOI for $750k AND asked the sellers to replace the roof before we would close.

Basically trying to buy the building for $500k with a new roof.

They countered at $1.2m, the full asking price, but they would replace the roof. We told the broker we weren’t interested and went silent for another month or two.

We got a call back from the broker again in 2019. He said they were desperate to make a deal.

They agreed and we signed a deal.

The sellers began doing the work of replacing the roof. Then COVID hit and everything slowed down. We sat and waited for 5 months.

I then convinced my bank to loan 67.5% LTV at 3.5% with 12 months of interest only. We ordered an appraisal and it came back at $1.85 million.

The environmental report came back and the sellers had to do about $15k of remediation to remove asbestos and some oil barrels in the basement.

Sources of funds at closing were as follows:

My bank: $950k

Sellers: $300k

Purchase Price: $1.2MM

On closing day we were wired $50k into our account and got ownership of a self-storage facility with a new roof and $15k a month of NOI.

That’s an in-place 15% cap rate. (Not sure what cap rate means? Take this free quiz).

Work we did after closing:

New security system ($12k)

Automatic / wifi overhead doors ($5k)

12 hr / 7-day access

No office (keeping manager on the team though, now she manages several facilities)

25% rent increase to get every customer up to market rate

9,000 sf of additional storage built in the building (opened in March 2022)

So how did it go?

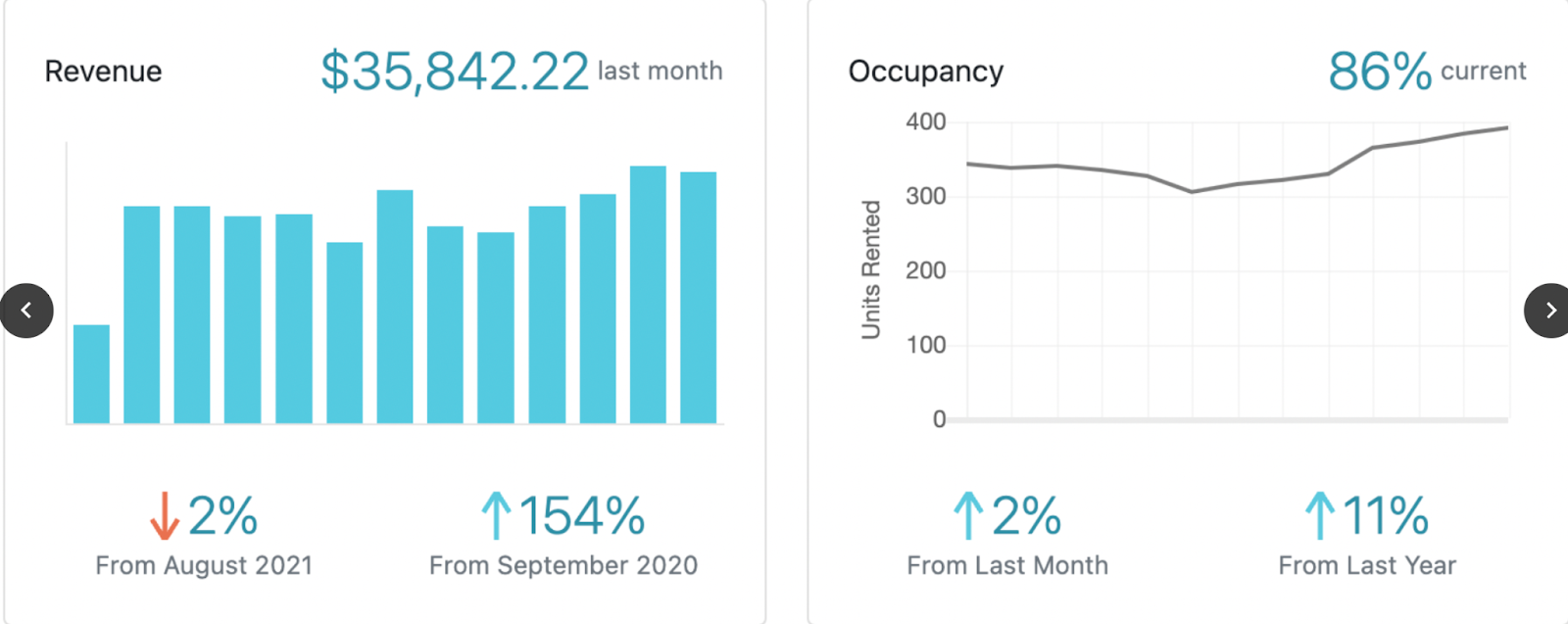

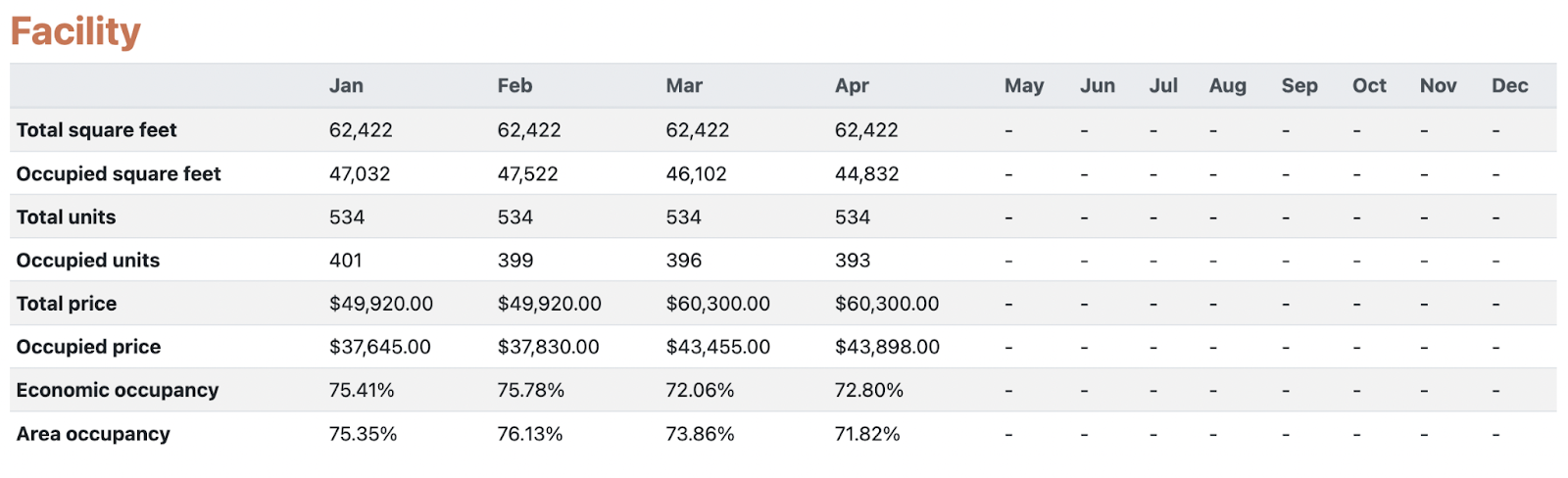

Great. Here is our first year of occupancy (screenshot as of September 2021:

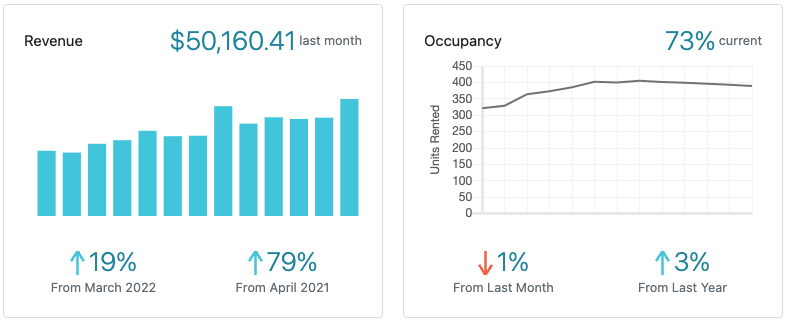

And into the winter / fall up to today:

We brought another 9,000 SF of storage online last month (prior to that we were 96% full).

The facility was mismanaged and there were a lot of non-paying customers that needed to be auctioned. Others also moved out because of the price increase.

Our occupancy dropped from 344 units at acquisition to 304 units in March of 2021 before ramping back up to 86% occupancy today.

Revenue jumped from $24k up near $29k before dropping back down to $26k in March. Then summer went really well with rentals and we have $37k on the rent roll as of October 1st.

How about our profitability?

2021:

So far in 2022:

We went from $25k on the rent roll at acquisition to $43k on the rent roll today. We also have 90% of our customers on a tenant insurance program and collect a few grand more per month in fees. Things are really rocking at this facility!

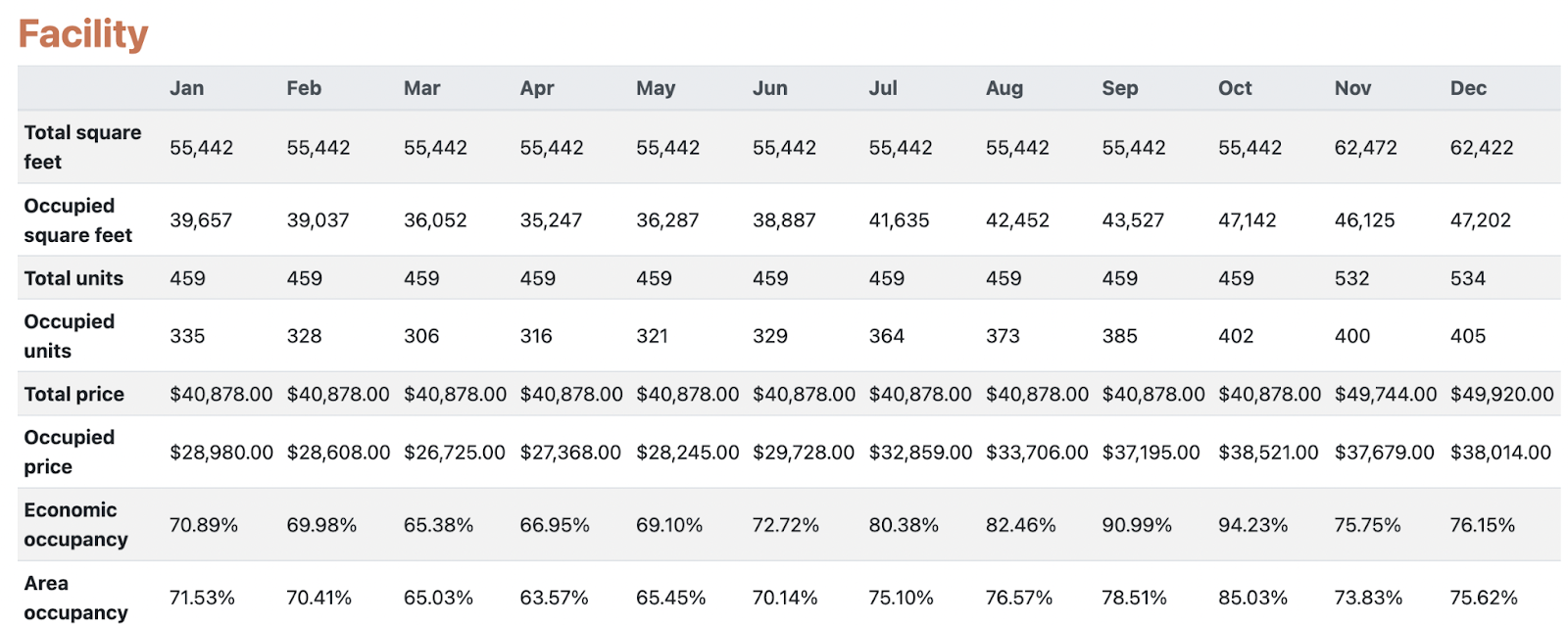

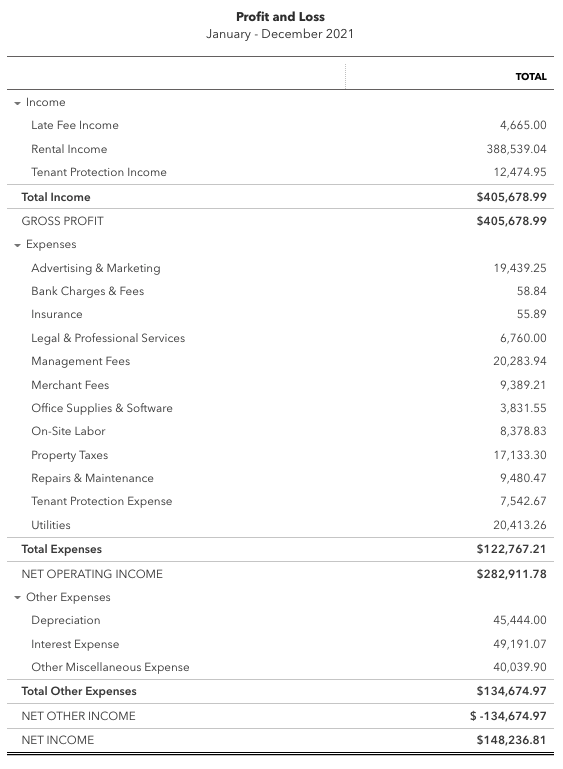

How about profitability? Here is our P&L for 2021:

But as you saw on the revenue report the facility is now generating $50,000 per month in revenue, or $150k per quarter moving forward.

That’ll all head to the bottom line for an annualized revenue figure of $600,000 and $150,000 in expenses. $450,000 of NOI is scheduled for the next 12 months.

How much value did we create?

Well the tailwinds behind storage are significant and over the past year and half since we negotiated this deal the market cap rates for storage units have compressed (something we never plan for but happens when investor appetite increases).

We could sell it right now at a 6 cap, or $450k in NOI / .06 = $7.5 million.

We acquired it for $1.2 million and now it’s worth $7.5 million.

This deal was a unicorn. It’s a bit unique and tough to manage. It’s in a small town and the market wasn’t like it is now back in 2019. For these reasons my partner and I did this deal with no outside investment, so we own 100% of the deal and the upside.

We got lucky and hit it out of the park with this one.

We didn’t want to sell it and pay capital gains (and we haven’t filled the newly constructed section so we went to our banker and pursued putting more debt on the property.

Now what I’m about to tell you about is the holy grail of real estate investing: the cash-out refinance.

When it comes to commercial real estate, the bank doesn’t value a property based on comparable sales or what you paid for it, they care how much money it is making and they work backward from there to assign a value.

The big bump in revenue (from $40k a month to $50k a month) was recent, so the bank wouldn’t underwrite that as the new value just yet. We had to use a trailing 6 months profit and loss statement that put our value a bit lower. We signed a term sheet and the bank ordered an appraisal and got started.

The value came back at $6 million.

The terms were 65% LTV, 2 years I/O, fixed rate for 5 years at 4.95%, amortizing over 25 years, personally guaranteed with a 5-3-1 prepayment penalty.

65% of $6 million is $3,900,000 in new debt.

We used the cash to pay off the $950k of previous debt & $300k of seller financing – and we had $2,650,000 leftover.

It was deposited into our checking account on Friday of last week. What a home run! And since we didn’t have a transaction beyond more debt, it wasn’t a taxable event. We’ll use the cash to co-invest in more deals and invest further in our acquisition pipeline.

The crazy part (and why we didn’t sell):

The Net Operating Income on the property is currently $450k and we’ll have $191k in debt service per year for the next two years. So not only did we just get this huge capital infusion from the new debt but the property will spit off $259k in cash over the next 12 months (over $10k each, per month, for my partner and me).

We’re also working with banks to get term sheets on another 10 of our properties that we acquired about a year ago which are now worth significantly more than what we paid for them.

They’ll all be total cash-out refinances (meaning we pull all of our equity out and return it to our investors) less than 18 months after acquisition. None of them will be quite as sexy as this one, but our $16 million acquisition in April is now worth north of $25 million now and we’ve got more room to run this spring.

We’ve now acquired just a hair over $75 million worth of self-storage and the total value at a 6 cap on current revenue figures is north of $150 million.

The last year has been a wild ride and we’re just getting started!